A Tale of Two Swiss Banks

A Tale of Two Swiss Banks

Unraveling 150 Years of UBS and Credit Suisse's Shared Heritage.

“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of light, it was the season of darkness, it was the spring of hope, it was the winter of despair.”

― Charles Dickens, A Tale of Two Cities

In the world of finance, there are certain images and narratives that persist, coloring the landscape with an air of exclusivity and prestige. One such image is that of Swiss banks, their vaulted halls catering to the needs of the wealthy elite, providing bespoke services for those with a taste for luxury. And within this lofty environment, two giants have long stood as pillars of the global financial system: UBS and Credit Suisse. Their head qarters situated a mere 300 yards apart in Zurich, fate has recently sent these two behemoths on strikingly divergent trajectories. UBS shares climbed an impressive 15% in the past two years, and they posted a profit of $7.6 billion in 2022. Credit Suisse, in contrast, has found its shares plummeting by 84% over the same period, and posted staggering loss of $7.9 billion in 2022.

The seeds of Credit Suisse's downfall were sown in 2021 (and probably even earlier, as can be seen soon), when the collapse of Archegos cost the bank a staggering $5 billion. This calamity set in motion a chain of events that would ultimately lead to a fire sale, culminating in the historic bank's acquisition by its erstwhile rival, UBS, for a paltry $3.2 billion in a deal supported by FINMA on March 19, 2023.

But what is it that led these two titans, with their parallel origins and shared ambition, to such radically different fates? For UBS and Credit Suisse, it is a tale of resilience and adaptability, of ambition and hubris.

Two Promises

“And a beautiful world we live in, when it is possible, and when many other such things are possible, and not only possible, but done-- done, see you!-- under that sky there, every day.”

― Charles Dickens, A Tale of Two Cities

In the intricate tapestry of Swiss banking history, there are moments and individuals that stand out, forever shaping the destiny of institutions and the financial landscape. One such luminary is Alfred Escher, a visionary of his time, whose insight and determination in 1856 led to the founding of the Schweizerische Kreditanstalt, the very institution that would later become the renowned Credit Suisse. Escher's ambitions were grand; he sought to catalyze Switzerland's industrial development and propel its economic growth into the modern era. This path culminated in a momentous merger with SKA, the third-largest Swiss bank at the time, in 1993. Through this strategic alliance, Credit Suisse solidified its domestic presence and fortified its standing within the Swiss retail banking sector.

In a parallel narrative, the origins of UBS Bank can be traced back to a mere six years after Credit Suisse's inception, with the establishment of the Bank in Winterthur in 1862. A pivotal moment in the bank's evolution occurred in 1912, when it merged with Toggenburger Bank, thereby laying the foundation for the Swiss Banking Corporation (SBC). This historic union set the stage for the expansion of SBC's global presence and ultimately paved the way for the emergence of the modern-day UBS Bank. The transformative year of 1998 bore witness to another seminal merger, this time with the Union Bank of Switzerland, which catapulted UBS Bank to the lofty position of Switzerland's largest bank.

The Night Shadows

“There is prodigious strength in sorrow and despair.”

― Charles Dickens, A Tale of Two Cities

Credit Suisse and UBS have been at the center of the financial world for over 150 years, enduring myriad storms and transformations. Their storied histories have been punctuated by two world wars, the Great Depression, the dot-com bubble, and the global financial crisis.

The crucibles of the First World War subjected both banks to treacherous economic landscapes. Switzerland's neutrality granted it the unique opportunity to become a financial center for international trade. Amidst the chaos, Credit Suisse and UBS demonstrated their adaptability, navigating the ever-shifting tides of war and geopolitics. As the banks survived and thrived, they played pivotal roles in reconstructing Switzerland's economy and establishing the Swiss franc as a bastion of stability. The World War II particularly had the Swiss banking sector ensnared in a complex web of geopolitical intrigue. Surrounded by Axis powers, the banks walked a tightrope of neutrality, balancing the suspicions of the Allies against the demands of their neighbors. They went so far as to hide their assets from the Axis powers by secreting their gold reserves to clandestine locations, demonstrating a remarkable resilience and commitment to their principles. UBS and Credit Suisse also covertly supplied Allied intelligence agencies with invaluable information on the Axis powers' financial transactions. UBS, for example, divulged details about German businesses and individuals with accounts in Swiss banks, thereby enabling the Allies to track the financial movements of their adversaries.

The dawn of the 21st century brought a new breed of challenges to the banking giants. The dot-com bubble's burst forced both banks to reconsider their strategies and reshape their businesses. You'd think that both banks learned some important lessons about risk management and the importance of diversification, that would have helped them handle the Global Financial Crisis (2007-2008) that followed.

They didn't.

Both UBS and Credit Suisse had significant exposure to toxic assets such as mortgage-backed securities and collateralized debt obligations (CDOs). (If you are unfamiliar with the whole subprime story, nobody explains it better than Margot Robbie, sipping champagne in a bubble bath.) UBS posted a loss of more than $20Bn in 2008 and had to be bailed out by the government. Arguably, the public anger at the Swiss authorities' 2008 rescue of UBS with government funding, may have nullified such rescue of Credit Suisse in Mar 2023.

The years that followed were marked by a series of scandals, ranging from tax evasion controversies to rogue trading and interest rate manipulation. Let’s list a few here:

Espionage Scandal (2019-2020): Credit Suisse internal issue; former COO hired private investigators to track ex-wealth management head; resulted in resignations and scrutiny of corporate culture.

Mozambique "Tuna Bond" Scandal (2016): Credit Suisse and others involved in financing state-owned companies; controversial $850 million bond led to financial instability, investigations, and criminal charges.

Forex Manipulation Scandal (2014): UBS and other banks implicated; agreed to pay $800 million in fines to various regulators; raised questions about market integrity and internal controls.

Libor Manipulation Scandal (2012): UBS among banks found manipulating LIBOR; paid $1.5 billion in fines; faced reputational damage, and employees charged with conspiracy and fraud.

Rogue Trader Scandal (2011): UBS rogue trader caused $2 billion loss; led to CEO resignation and concerns about risk management practices.

The Tax Evasion Controversy (2008 -2014) subjected UBS and Credit Suisse to intense scrutiny. They faced allegations of assisting wealthy clients in evading taxes using secret Swiss bank accounts. In 2009, UBS paid a $780 million fine to the U.S. government, disclosed information on U.S. clients, and avoided criminal prosecution. Similar tax evasion allegations surfaced in France, Germany, and Belgium, leading to more fines and settlements. In 2014, Credit Suisse pleaded guilty to conspiring to aid tax evasion and agreed to pay a $2.6 billion fine to U.S. authorities, marking the first time in decades a global bank had pleaded guilty to criminal charges in the United States.

These events brought scrutiny to the banks' corporate cultures and governance practices, raising questions about their ethical standards and internal controls. Despite these setbacks, Credit Suisse and UBS persevered, adapting to the new regulatory environment and implementing reforms to prevent future misconduct.

The Sea Still Rises

“Nothing that we do, is done in vain. I believe, with all my soul, that we shall see triumph.”

― Charles Dickens, A Tale of Two Cities

And in between these challenges, UBS and Credit Suisse also managed to expand their business beyond Europe. The first to make a move was Credit Suisse. In 1978, Credit Suisse acquired a majority stake in the First Boston Corporation, a leading American investment bank. On one hand, the partnership signaled the dawn of a new era of growth and global expansion. On the other, it presented the challenge of bridging two distinct corporate cultures and financial markets. The successful collaboration bolstered Credit Suisse's standing as a powerhouse in the world of finance. The acquisition marked a significant expansion of Credit Suisse's investment banking operations, especially in the United States. However, when the bubble burst in the early 2000s, investment banking revenue declined sharply, putting pressure on both banks' profit. The bank merged its investment banking division with First Boston to form Credit Suisse First Boston (CSFB), solidifying its position in the global investment banking market.

UBS acquired PaineWebber in 2000, a leading U.S. brokerage firm, significantly expanding its wealth management presence in the United States. The acquisition helped UBS diversify its business and establish a strong foothold in the U.S. market. This was around the same time UBS expanded its wealth management operations, catering to high-net-worth individuals and families, and institutional clients.

They focused in the growing Asia markets as well , UBS expanded its wealth management operations, targeting high-net-worth individuals, families, and institutional clients. By focusing on key growth markets like China, Singapore, and Hong Kong, UBS has become one of the leading wealth management firms globally, further strengthening its position as a global financial institution. Credit Suisse to follow the lead to mark their presence in Asia.

Between 2010 and 2022, both UBS and Credit Suisse implemented various strategies to optimize their operations and run profitable businesses. Their key efforts included a focus on core businesses, cost reduction, expansion in key markets, and improved risk management. While both banks pursued similar goals, their approaches differed, with UBS placing greater emphasis on wealth management and downsizing its investment banking operations, while Credit Suisse opted for a more balanced approach between its wealth management and investment banking businesses. In the end, the key factor to Credit Suisse's lower performance was that between 2008 and 2023, investment banking arm underperformed, dragging down the business's profitability and causing significant losses.

A Knock at the Door

“Tell the Wind and the Fire where to stop; not me.”

― Charles Dickens, A Tale of Two Cities

In the spring of 2023, before the frenzy of March Madness gripped basketball fans, a different kind of madness unfolded in the financial world. A series of dominoes began to topple, causing a chain reaction of bank failures that shook the financial sector to its core.

The first domino to fall was Silvergate Bank. Founded in 1988 as a humble savings bank, Silvergate took a bold leap into the world of cryptocurrency in the 2010s. By the end of 2022, a staggering 90% of the bank's deposits were tied to cryptocurrency, much of it in FTX. However, when FTX went bankrupt, panic ensued, and Silvergate faced a devastating bank run. On March 8th, 2023, Silvergate Bank chose voluntary liquidation as its only option.

But Silvergate was just the beginning.

Two days later, the storied Silicon Valley Bank also collapsed due to a bank run. The tale of its downfall has been widely discussed, so I will spare you the gory details. You can find a concise summary here. Just when it seemed the worst was over, on March 12th, 2023, Signature Bank from the east coast was almost temporarily closed by regulators. In a last-ditch effort to stave off disaster, a $30 billion lifeline was thrown by JPMC, BoA, Wells Fargo, Citigroup, and Truist. A crucial meeting between US Treasury Secretary Janet Yellen and the CEOs of these banks helped to prevent the bank's total collapse.

The shockwaves from these failures rippled through the financial sector, impacting other banks such as First Republic Bank, whose shares plunged by as much as 52%. To address the mounting crisis, the Federal Reserve announced an emergency lending program to help banks meet depositor demands and avoid having to sell off assets during this tumultuous time.

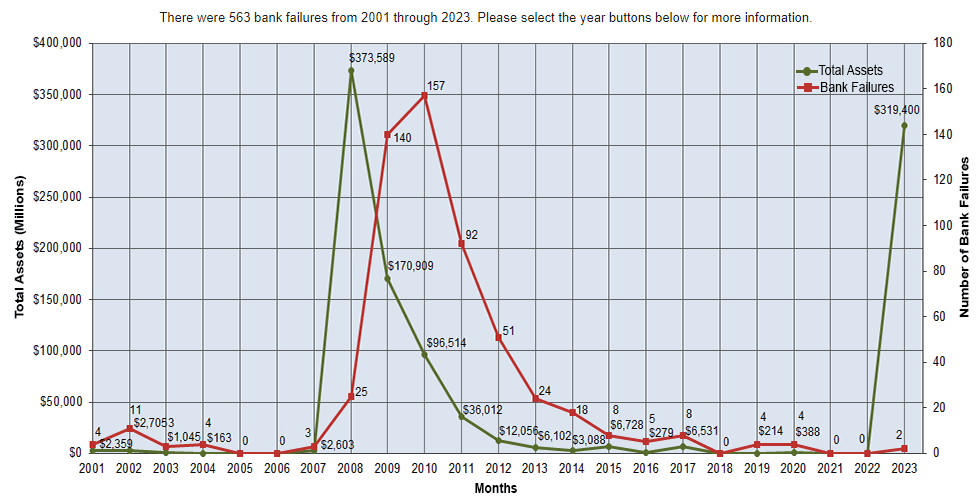

Now, the question arises: how unprecedented was this triple bank run in March 2023? It's easy to see it as a financial doomsday, but the reality is that bank failures have become increasingly common. Between 2011 and 2023, the US alone witnessed a total of 563 bank failures. The subprime crisis of 2008-2009, in particular, saw a staggering 140 bank failures in 2009 and 157 in 2010. You can explore these sobering statistics on the FDIC site here.

The Footsteps Die Out Forever

“I see a beautiful city and a brilliant people rising from this abyss." ― Charles Dickens, A Tale of Two Cities

As the troubles across the Atlantic raised concerns about the banking industry's next weakest link, all eyes turned to Credit Suisse. We had seen that the bank was already ailing, and in Q4 2022, clients pulled nearly $119 billion from the bank.

On 15th of March, Ammar Al Khudairy - Chairman of Saudi National Bank - the largest shareholder owning 9.9% of Credit Suisse stated "The answer is absolutely not" as an answer to if SNB would make additional investments in Credit Suisse. Al Khudairy had good justifications (capital requirements prevented it from holding more than 10%), but he might as well as said "beware the Ides of March" at this point. Credit Suisse stock plunged to the lowest level on record wiping out the value of Saudi National Bank’s investment along with it. Al Khudairy resigned two weeks later "due to personal reasons".

The tide of withdrawals rose as high as $10 billion in a single day.

In the Swiss financial industry, apparently there’s an expression "It would be like UBS and Credit Suisse merging" - a joke to indicate the unlikelihood of something happening. However it is said that Tidjane Thiam, Credit Suisse CEO from 2015 to 2020, often discussed the idea with colleagues, and as Credit Suisse weakened, UBS executives said to have contemplated the idea of how to acquire its rival, and what governmental help it would need. Now, regulators feared that Credit Suisse would be insolvent if the issue is not dealt with. Credit Suisse was told "You will merge with UBS and announce Sunday evening before Asia opens. This is not optional".

On Saturday, UBS had offered to buy Credit Suisse for roughly $1 billion. Credit Suisse's board rejected the offer, them arguing that its real estate holdings alone were worth around that amount - but ultimately capitulated to a $3.2 billion government-backed deal. Swiss National Bank extended a loan of $108 billion to both banks to boost liquidity. Rumors swirled that BlackRock had been interested in acquiring Credit Suisse, but Swiss authorities preferred a domestic solution, and the shadow of UBS loomed large (UBS is a major customer of BlackRock).

The plot thickened when the Swiss Financial Market Supervisory Authority (FINMA) agreed to wipe out $17 billion worth of Credit Suisse's AT1 bonds. AT1 (Additional Tier 1) bonds are a riskier variety - they may be converted to equity or written down in certain situations. The outcry was however due to the decision upending the traditional pecking order of bondholders and shareholders. The ECB (The European Central Bank) for example, sought to distance themselves from this decision and in fact made a statement that they will continue to impose losses on shareholders before bondholders as is the common practice.

And so, after a 167-year run, Credit Suisse met its fate, not as the willing Dickensian hero Sydney Carton, but as a casualty in a high-stakes financial drama. The employment guillotine would certainly fall, but the greater concern is the damage to Switzerland's reputation as a safe haven for investment. This is a serious hurdle for a country with high reliance on finance for its economy.

The loss of Credit Suisse, the bank that once bankrolled Switzerland's railways, leaves a deep scar on the nation's financial landscape. Yet, we must remember that every end is a new beginning. The acquisition would make UBS stronger, solidifying its position as a leading global wealth manager and Swiss universal bank. UBS is poised to become the world's leading wealth manager, boasting $5 trillion in invested assets.

In the words of Dickens, "It is a far, far better thing that I do, than I have ever done." Let us hope that the lessons learned from Credit Suisse's demise will lead to a brighter, more resilient future for the world of finance.

note: all images are generated by DALL-E, via Bing.

Did this spark your interest? Please hit that like button, share with your friends, and subscribe to my Substack newsletter. I regularly explore topics like leadership, philosophy, technology, startups, and angel investment, and I'd love to have you on board.

Your feedback is essential in shaping this journey, so please don't hesitate to engage with me. Let me know what you enjoyed and what I can improve by leaving a comment or sending a message.